We believe the world economy is now entering the next phase of the cycle. H2 2023 should be more clearly characterised by slowing growth, falling inflation, and a peak in central bank policy rates. Yet, the underlying resilience of the global economy (with still tight jobs markets) suggests interest rates will be held higher for longer as only a mild recessionary backdrop delivers a more gradual decline in inflation from here. Modest rate cuts are likely a 2024 story, while renewed geo-political tensions remain a risk for later in the year.

In this month’s Core Offerings, we outline our key calls for H2 2023 across economies, markets, and portfolio construction. We retain our strong overweight to fixed income relative to equities, and believe the former is likely a multi-year view. As we approach the end of the rate-hiking cycle, there are increased odds of a ‘soft landing’ globally. Although this is not our central case, we have closed our modest underweight to equities (and high yield credit). We continue to favour quality and non-US equity markets, including Australia.

“The world is flooded with confusion and change. The S&P 500 Index and the US economy have defied consensus pessimism this year. Investment hype surrounding artificial intelligence (AI) has gone manic.”

Sometimes things change a lot and sometimes they change a little. That’s the nature of life, and often the nature of markets and economies. And over the past couple of months —deep winter in Australia and a holiday season in the northern hemisphere that many Aussies seemed to have availed themselves of—some things haven’t changed that much.

This would include the resilience of the global growth picture, with the much-heralded global recession of H1 2023 failing to appear in any great measure. The same would apply to Australia, where the mid-year housing mortgage reset avalanche is only just starting to reveal itself in changed consumer buying patterns and weaker retail sales. Of course, global growth did approach a near-recessionary pace of 2% in late 2022. But only a mild recession in Europe and resilient growth in the US, together with an arguably faltering rebound in China, have steadied global activity closer to a sub-trend 3% pace in H1 2023. Jobs markets globally have remained stubbornly tight, with unemployment rates near 50-year lows. They show little response to steadily rising interest rates in virtually every key economy, and the fastest pace of rate increases in 40 years for Australia and the US.

Some things have changed a lot, however. One of those is the pace at which inflation has been moderating, together with clearer signs core inflation is easing. This is especially true in the US and Australia, and tentatively in Europe and the UK. Those expecting a hard landing for the world economy—and a sharp retracement in risk assets—frequently point to the stickiness of core inflation to claim the notion of ‘immaculate disinflation’ as falsehood, with the necessity of a sharp rise in unemployment to bring salvation to the inflation outlook.

This debate is hardly over. Growth seems destined to slow further as the impact of credit tightening weighs. But the comfort central banks are likely to have garnered from the recent faster pace of inflation moderation (even if most of easier gains are behind us), does increase the chances that they are at the peak of their respective rate-hiking cycles. A peak in rates is likely to happen by September in Australia and the US, and by year-end in Europe and the UK. Indeed, emerging market central banks are already cutting rates, with more to come as the rest of the year unfolds.

There also remain grave concerns that inflation will only reach central banks’ target ranges after an extended period of sustained high interest rates. This will challenge the ability of risk assets to leap higher, as they sometimes do when central banks reach their

“It may well be a “jobloss-less” recession, where growth, spending, and investment contract modestly, but unemployment rises barely above 4%. This is not much different from what a soft landing would look like.”

This month we close our small underweight to equities. We have maintained a mild recession view for some time, and that may still eventuate over the coming year. However, the faster pace of inflation moderation (and somewhat resilient growth) increases the likelihood that peaking central bank tightening underpins a softer landing for growth.

As UBS recently penned for the US economy, it may well be a “jobloss-less” recession, where growth, spending, and investment contract modestly, but unemployment rises barely above 4%. This is not much different from what a soft landing would look like”. This may well be a theme persisting across many economies over the coming year.

Despite this move, we prefer some non-US equity markets, such as Australia and emerging markets, but retain a strong preference for fixed income over equity returns. On the following pages, we outline our key macro and tactical calls for the rest of this year.

“It has been a full year since the US leading economic indicator turned negative on a year-over-year basis…from this perspective, it is genuinely surprising that the US economy has not yet tipped into a recession.”

The past year has been characterised by high inflation that has corrected lower by less than expected, together with persistent monetary tightening. Looking ahead to H2 2023, growth is slowing, inflation is falling, and thus we expect interest rates to peak. With more work to do on returning inflation to central bank targets, a key defining feature of this new phase is that interest rates are likely to be held higher for longer than in prior periods.

We continue to view the global outlook as one of mild recession, notwithstanding it is likely to have elements of a ‘soft-ish landing’. At times, concerns of a harder landing may also emerge. Jobs markets remain tight, and thus supportive. However, the lagged impacts of rapidly tightened credit conditions are yet to fully weigh (as we discussed in June’s Core Offerings, Central bank outlook—Skip, hike or pause as cuts delayed to 2024).

Reflecting this, and as discussed below, while equities typically start to appear favourable as growth reaches its nadir, their valuations, which can at best be described as fair, leave them tactically neutral. Still, a horizon promising lower rates and lower inflation cautions against an overly pessimistic view given our six to 12-month tactical timeframe. When rate cuts eventually come—most likely in 2024—interest rates may linger at or above neutral (or normal) until central banks feel comfortable the war has been won. A return to uber-easy rates seems unlikely without first experiencing more unemployment than is now expected.

The renewed escalation of geo-political events is also likely to feature in the period ahead. This includes potential shorter-term escalations in H2 2023 that caution against adding too much risk, given the vulnerability current equity valuations embody. It also plays into the longer term, where shifting global alliances and periodic trade wars underpin a steady re-adjustment of supply chains. Added to this are other factors (such as labour shortages) that support our long-held view that inflation is unlikely to trend near the lows of the past decade.

One key area of geo-political tension is the ongoing war in Ukraine. A ceasefire toward year-end is possible, though this is likely to require escalation around a Ukraine offensive. And too great a victory could increase the chances or irrational actions from Russia. Another key area is Iran, seen by BCA Research as “one of the most underrated geopolitical risks”. With the prior ‘Iran nuclear deal’ inactive, Iran now has the capacity to enrich its stockpile of uranium to weapons-grade levels, with estimates suggesting that the stockpile is large enough to create five nuclear weapons in one month.

“The war will escalate due to Ukraine’s counteroffensive and become relevant to investors again in the second half of 2023, likely causing significant equity volatility.”

“The biggest pricing anomaly in the fixed income markets is the U.S. yield curve, more extremely negative than at any time in modern history except for the early 1980s.”

Often in history, central banks have found themselves reversing prior rate hikes quickly post their peak. Sometimes this is because the extent of positive momentum in growth and inflation is so strong that finding the appropriate peak requires ‘breaking something’. At other times, central banks face shocks that were, by definition, unanticipated. This can lead to rapid performance for fixed income, as markets reprice the outlook for multiple rate cuts.

Looking ahead, this is a plausible scenario, should we find that central banks have already done enough to provoke a deeper-than-expected recession (most likely through the credit channel), or inflation unexpectedly reverses higher, requiring more significant tightening.

However, given our base case of falling inflation and only a mild economic downturn, it’s likely our overweight to fixed income will deliver moderate returns over a number of years, rather than a short, sharp profit. This largely reflects our view that part of the ‘new phase’ is inflation settling at a higher resting place, not well below central bank targets as in the past. Shifting supply chains, ageing workforces, and the energy transition are all factors likely to limit inflation’s ability to return to rates below central bank targets.

In this scenario, central banks are likely to cut rates in 2024, but only toward or above neutral. This lends itself to less aggressive outperformance of fixed income than would otherwise be the case in a sharper downturn—but it is also a less positive outlook for equities, given valuations.

Central banks are likely to cut rates in 2024, but only toward, or above, neutral. This lends itself to less aggressive outperformance of fixed income than would otherwise be the case in a sharper downturn—but it is also a less positive outlook for equities, given valuations.

The postponement of US recession risk, clear signs of peak inflation, and the closeness of peak monetary policy, have prompted investors to abandon recession trades. Equities are focusing on stronger-than-expected growth and softer-than-expected inflation via a cyclical, growth-led rally.

The thesis is that inflation is decoupling from growth, allowing for a more supportive backdrop to corporate earnings. With less aggressive interest rate moves and, consequently, higher valuations, the one year forward price/earnings (P/E) ratio for global equities is now 17.5x. This is a level that would have been considered ‘peak’ prior to COVID. A key question for H2 2023 is whether growth and inflation recouple, resulting in central banks staying restrictive for longer. Alternatively, central banks could gain enough confidence to outline a path of easier monetary policy in 2024.

Looking ahead, dwindling excess consumer savings will meet lower inflation pressures and improve purchasing power. The relative importance of each to the consumer will be a key determinant in how equity markets perform in the face of 4-5% cash rates.

Our neutral equity stance is governed by this uncertainty and a preference for value-orientated markets—i.e., we favour Australia and emerging markets versus the US and Europe. We still favour later-cycle, defensive exposures, under-levered balance sheets, and sectors exposed to higher-for-longer rates (e.g., insurance). Once greater clarity on the above questions emerge, investors may need to adjust their cyclical/growth exposures.

“The difference in performance between the S&P 500 and the equal-weight index, broadly-defined tech sector outperformance – driven by extreme optimism about the potential for AI products to meaningfully boost tech sector earnings growth – has accounted for the majority of the outperformance of US stocks versus bonds.”

So far this year, a potentially peaking US Federal Reserve (Fed), fundamental earnings (and economic) resilience, and a new longer-term growth engine via generative AI have all contributed to performance. Yet, valuations are increasingly putting pressure on the mega-caps to deliver on implicit growth expectations.

Much has been made of the ‘narrow’ leadership of US equities year-to-date. To some extent, an optically expensive S&P 500 (almost 20x 12-month forward P/E) is misleading. Whilst mega-cap tech trades at forward multiples not far removed from COVID highs, an equally weighted S&P 500 trades on a much more reasonable 16x.

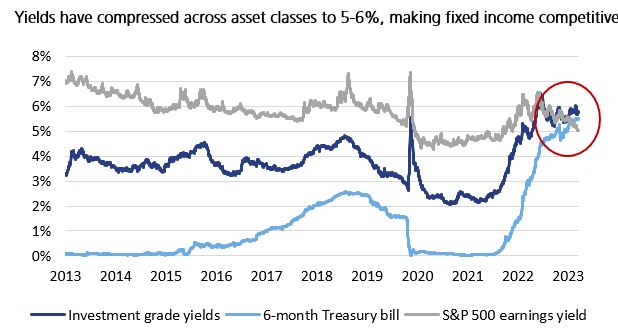

Nonetheless, investors are being confronted with a new reality—with the S&P 500 offering an earnings yield of just 5%, they can earn better yields on the risk-free six-month government bond and investment grade credit (which are currently yielding 5.5% and 5.8% respectively—see chart on previous page). This reversal of conventional finance, whereby investors are seemingly demanding little to no risk premium for investing in US equities, suggests that forward- looking return expectations should be tempered.

Ample diversification, rebalancing, quality, and active management will be key pillars of portfolio construction going forward.

Some of the key challenges to solve moving forward are potentially prolonged volatility, persistent inflation, heightened default risks as valuations adjust to a permanently higher levels of interest rates, ongoing multiple expansion resulting in heightened (but vulnerable) valuations, and narrow leadership as investors scavenge for growth.

With this in mind, it is prudent to construct portfolios with resilience to these elements, but to also ensure that portfolios can still capture opportunities in high dislocation environments. Ample diversification, rebalancing, quality, and active management will be key pillars of portfolio construction going forward.

Equities: Portfolios should avoid factor build-up, particularly after the recent strong run in growth equities. Diversifiers should be introduced, such as style-neutral or value strategies with lower exposure to mega-caps in favour of underrepresented or undervalued parts of the market. Portfolios should also lean into regions where valuations are less extreme.

Fixed income: Adding duration via high grade bonds, which offer higher yields for relatively low risk, can provide a ballast to portfolios. Credit (including in private markets) should play a more significant role, now there is more adequate compensation for risk. Given interest rates may stay elevated for longer, a bias toward quality is recommended.

Alternative assets: Assets with inflation linkage, such as real assets, provide inflation protection. Infrastructure is our most favoured sub-asset class as it can provide more defensively positioned core assets on long-term, typically inflation-linked contracts. This can provide both a defensive ballast and inflation protection, both of which are in high demand.

In the new phase, it is paramount to embrace active management to avoid a build-up of risk and capture dislocations. Active managers have the ability to add significant value in this environment. Additionally, quality will be important. It is prudent to trim lower quality exposures that have rallied, as a high-rate environment could lead to heightened financial stress and defaults.

We have made three active decisions this month, in addition to remaining overweight fixed income relative to equities, which is core to our current positioning:

Indeed, from an investment cycle perspective, the time to adopt a maximum underweight in equities is typically following the first few rate hikes, not at the end of rate cycle, as now appears to be emerging. Given the ongoing debate between hard landing, soft landing, and no-landing, harvesting tactical alpha in fixed income, where confidence levels are greater, seems prudent.

While the high-yield sector is vulnerable to tightening financial conditions, which can lead to higher defaults, we have closed our modest underweight to this sub-sector, as running yields are likely to compensate for a modest re-widening in spreads (relative to equities). We retain our preference for investment grade on a risk-adjusted basis.

Although growth is slowing, it is still positive, with jobs markets remaining tight. Core inflation is continuing to slow, and there are expectations that global credit markets will continue to tighten.

Our views have changed to reflect a move closer to peak interest rates and slowing inflation. We retain an overweight to fixed income, as we expect it to perform well relative to equities under several scenarios in the short term, but we have moved our equities underweight to a neutral position.

Inflation volatility is likely to persist—Inflation continues to fall, though services inflation remains sticky. However, fading impacts of globalisation, structurally tight labour markets, and geo-political impacts on supply chains suggest less deflation and more inflation.

A return to ‘normal’ interest rates—Peaking inflation is likely to foster a near-term peak in central bank hikes. But stickier inflation than over the past two decades is likely to limit a return to near-zero interest rates.

Geo-political volatility likely to be enduring—Russia’s invasion of Ukraine has ended a long period of benign globalisation. Ongoing decoupling of leading-edge technology, political and trade alignment, as well as military and energy security, are all key potential drivers of growth and profits.

Diversification matters—In a world of heightened volatility and fewer long-cycle trends, it is important to maintain portfolio diversification, avoiding over-exposure to individual markets, sectors and other specific return drivers. Unlisted investments are likely to grow in favour.

The energy transition—As the world faces a trade-off between net-zero commitments, cost, and energy security, this is setting the scene for both old and new forms of energy to play a role.

Sustainable investing—As the world becomes more connected, it is also becoming more socially aware. The intersection of finance and sustainability will govern a reallocation of capital.

The search for income—The exit of ‘zero-bound interest rates’ has resulted in a resetting of income expectations across all asset classes, including equities, fixed income, and income-generating unlisted assets.

Deglobalisation—Brexit, trade wars, COVID-19, and Russia’s invasion of Ukraine have up-ended a relatively harmonious world order, with impacts spanning geo-politics, military spend, supply chains and demographics.

| What we like | What we don't like | |

| Equities |

|

|

| Fixed income |

|

|

| Alternatives |

|

|

Read the full Core Offerings report here

About this document

This document has been authorised for distribution to ‘wholesale clients’ and ‘professional investors’ (within the meaning of the Corporations Act 2001 (Cth)) in Australia only.

This document has been prepared by LGT Crestone Wealth Management Limited (ABN 50 005 311 937, AFS Licence No. 231127) (LGT Crestone Wealth Management). The information contained in this document is provided for information purposes only and is not intended to constitute, nor to be construed as, a solicitation or an offer to buy or sell any financial product. To the extent that advice is provided in this document, it is general advice only and has been prepared without taking into account your objectives, financial situation or needs (your ‘Personal Circumstances’). Before acting on any such general advice, LGT Crestone Wealth Management recommends that you obtain professional advice and consider the appropriateness of the advice having regard to your Personal Circumstances. If the advice relates to the acquisition, or possible acquisition of a financial product, you should obtain and consider a Product Disclosure Statement (PDS) or other disclosure document relating to the product before making any decision about whether to acquire the product.

Although the information and opinions contained in this document are based on sources we believe to be reliable, to the extent permitted by law, LGT Crestone Wealth Management and its associated entities do not warrant, represent or guarantee, expressly or impliedly, that the information contained in this document is accurate, complete, reliable or current. The information is subject to change without notice and we are under no obligation to update it. Past performance is not a reliable indicator of future performance. If you intend to rely on the information, you should independently verify and assess the accuracy and completeness and obtain professional advice regarding its suitability for your Personal Circumstances.

LGT Crestone Wealth Management, its associated entities, and any of its or their officers, employees and agents (LGT Crestone Group) may receive commissions and distribution fees relating to any financial products referred to in this document. The LGT Crestone Group may also hold, or have held, interests in any such financial products and may at any time make purchases or sales in them as principal or agent. The LGT Crestone Group may have, or may have had in the past, a relationship with the issuers of financial products referred to in this document. To the extent possible, the LGT Crestone Group accepts no liability for any loss or damage relating to any use or reliance on the information in this document.

Credit ratings contained in this report may be issued by credit rating agencies that are only authorised to provide credit ratings to persons classified as ‘wholesale clients’ under the Corporations Act 2001 (Cth) (Corporations Act). Accordingly, credit ratings in this report are not intended to be used or relied upon by persons who are classified as ‘retail clients’ under the Corporations Act. A credit rating expresses the opinion of the relevant credit rating agency on the relative ability of an entity to meet its financial commitments, in particular its debt obligations, and the likelihood of loss in the event of a default by that entity. There are various limitations associated with the use of credit ratings, for example, they do not directly address any risk other than credit risk, are based on information which may be unaudited, incomplete or misleading and are inherently forward-looking and include assumptions and predictions about future events. Credit ratings should not be considered statements of fact nor recommendations to buy, hold, or sell any financial product or make any other investment decisions.

The information provided in this document comprises a restatement, summary or extract of one or more research reports prepared by LGT Crestone Wealth Management’s third-party research providers or their related bodies corporate (Third-Party Research Reports). Where a restatement, summary or extract of a Third-Party Research Report has been included in this document that is attributable to a specific third-party research provider, the name of the relevant third-party research provider and details of their Third-Party Research Report have been referenced alongside the relevant restatement, summary or extract used by LGT Crestone Wealth Management in this document. Please contact your LGT Crestone Wealth Management investment adviser if you would like a copy of the relevant Third-Party Research Report.

This document has been authorised for distribution in Australia only. It is intended for the use of LGT Crestone Wealth Management clients and may not be distributed or reproduced without consent. © LGT Crestone Wealth Management Limited 2023.